| Business rate reforms aim to support smaller retail assets but may unintentionally impact high-value offices and logistics buildings | Regional office rents reached record growth as ESG-compliant, prime stock remains scarce across major UK cities | Rising taxes on rental income may squeeze buy-to-let yields and prompt some landlords to reassess investment strategies |

Budget changes reshape the housing market

November’s Budget introduced several housing-related measures that could have lasting implications across the property market.

Landlords are set to face increased tax pressure. From April 2027, Income Tax on rental income will rise by two percentage points, lifting rates to 22% for basic, 42% for higher and 47% for additional-rate taxpayers. This is likely to reduce net rental yields for many buy-to-let investors at a time when costs are already elevated.

First-time buyers will also see change ahead, as the government plans to replace the Lifetime ISA. A consultation is expected in early 2026, with the aim of launching a simpler savings product to support home ownership.

Meanwhile, a new High Value Council Tax Surcharge will apply from April 2028 to homes worth £2m or more. Although affecting only around 0.5% of properties, mainly in London and the South East, it may influence wider market behaviour.

Tenancy reforms under the Renters’ Rights Act

The government has confirmed that the first phase of the new Renters’ Rights Act will come into force in May 2026.

The initial phase of the rollout will relate solely to tenancy reform, while other measures will take effect in two subsequent stages. From 1 May 2026, all fixed term tenancies will automatically convert to periodic tenancies, meaning tenancy agreements will no longer have a set end date. Tenants will be required to provide two months’ notice if they wish to leave a property. Meanwhile, landlords will no longer be able to serve Section 21 notices; instead, they will need to provide a valid reason when evicting tenants.

In addition, landlords will only be able to raise rent once a year and, when doing so, they must provide at least two months’ notice. Renters will have the right to challenge the increase – if they do, landlords will be prohibited from evicting tenants in response.

Great Britain’s happiest places to live

Rightmove has released its annual Happy at Home Index, revealing the happiest places to live in Great Britain.

This year, Skipton in North Yorkshire was awarded the top spot, with residents praising the market town’s access to nature and green spaces, proximity to essential services and the friendliness of the locals. London was home to some top-performing areas, with Richmond upon Thames and Camden in second and third place respectively. Harrogate, Woodbridge and Altrincham also feature in the top 10, along with Stirling in Scotland.

Rightmove surveyed residents from over 200 locations and found that one of the key drivers of happiness is a sense of belonging. A town’s safety and physical environment also play a significant part in residents’ happiness. Overall, the survey found that those living in the South West are most content with where they live, while residents of the East Midlands are least happy.

Business rate changes announced in Budget

In the Autumn Budget 2025, the Chancellor announced changes to the business rates system, which have been met with mixed responses across the industry.

From April 2026, eligible retail, hospitality and leisure (RHL) properties valued below £500,000 will benefit from lower tax rates – their standard multiplier will drop by 5p. To offset these reduced rates, properties valued at £500,000 or higher will see a 2.8p increase in the standard multiplier. The intention behind the increased rates was to target online retailers with large warehouses; however, some industry experts have expressed concern that other businesses will be affected too.

Ion Fletcher at the British Property Federation commented, “This is not, as the Chancellor suggested, a de facto tax on online retailers, it will hit all businesses in larger, high value buildings including manufacturing, life sciences and logistics businesses in warehouses, as well as financial and professional services based in modern office space.”

Regional offices see rapid prime rental growth

Prime rents in the UK’s regional office markets increased at a record pace this year, a report has found.

The data from Lambert Smith Hampton (LSH) shows that, in the 15 key regional office markets, prime rents are set to have risen by 8.2% in 2025. Growth is even stronger in the ‘Big Six’ markets (Birmingham, Bristol, Edinburgh, Glasgow, Leeds and Manchester), as prime rents are on track to have increased by 10.2% in 2025. In the first three quarters of the year, Leeds was the regional city that saw the strongest growth, with prime rents rising by 18%.

LSH attributed the record growth rates to increased demand for state-of-the-art offices that are ESG-friendly. But these top-quality spaces are currently relatively low in supply, so rents have increased significantly. At the moment, prime offices account for only 5% of total supply in the regional markets, which is down from 9% in 2023.

West End investment market update

Data from Savills indicates that October was a positive month for the West End investment market.

In October, investment in the West End market generated £437m – there were seven transactions in total, two of which were over £100m. This brings the number of £100m+ transactions this year-to-date (YTD) to nine, with a combined value of £2.2bn.

Overall, the cumulative value of West End investments this YTD is £4.3bn, meaning transactions above £100m represented over half of this year’s sales. Institutional investors accounted for 71% of this year’s transactions above £100m, highlighting that this group is targeting higher-value assets. The largest West End transaction of the YTD was the sale of 1 Newman Yard, W1 – the 121,252 sq. ft property was purchased by Royal London in October for £250m.

Looking ahead, Savills forecasts that total West End sales could reach £5.5bn by the end of 2025, notably higher than last year’s total of £4.4bn.

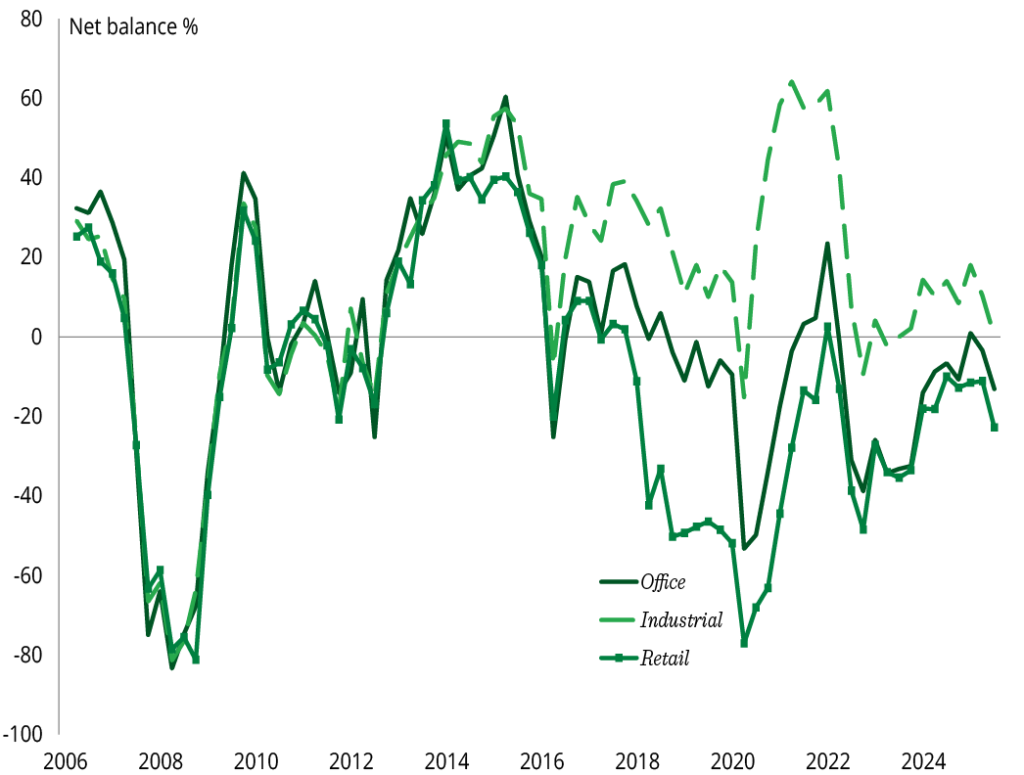

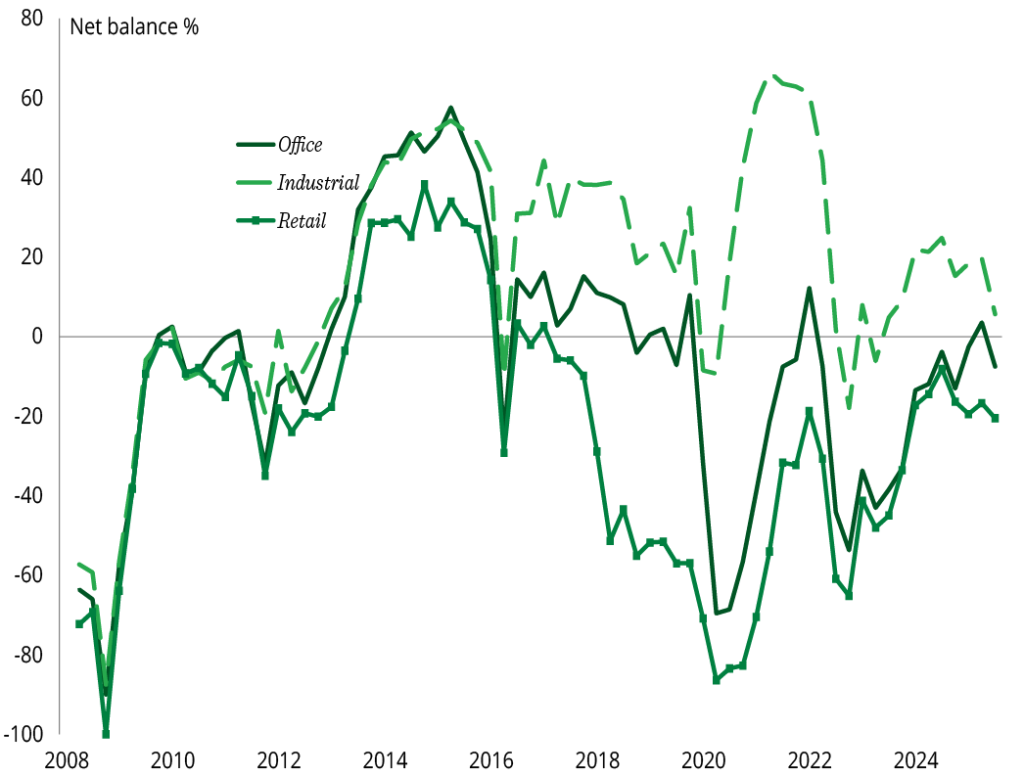

Commercial property outlook

Investment enquiries – broken down by sector

- The headline net balance for investment enquiries in Q3 2025 was -10

- Investor enquiries declined for office and retail assets

- There was stagnation of investment enquiries across the industrial sector.

Capital value expectations – broken down by sector

- Capital value projections were pared back across all categories

- Prime office and industrial values are expected to move marginally higher

- All other traditional sectors are expected to see some degree of decline in capital values over the coming year.

Source: RICS, UK Commercial Property Monitor, Q3 2025

All details are correct at the time of writing (17 December 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK.