| Housing outlook – Savills has predicted house prices will fall by 2% this year | Commercial market – data from Carter Jonas indicates an uneven recovery in investment volumes, below levels seen in Q4 2025 | House sales – according to Rightmove, 44% of UK homes for sale failed to sell in the last three years |

Revised outlook for 2026

Savills has revised its house price forecasts for 2026 in light of the ongoing conflict in the Middle East.

It is now anticipated that house prices will fall by 2% this year, with London and the South East seeing the biggest declines. The five-year forecast has seen less change, with some capacity for growth in the medium term. Markets have responded quickly to the economic shock caused by the geopolitical events, so prolonged conflict would pose a risk to the housing market.

There are high levels of stock on the market because buyer confidence has taken a hit and landlords are selling up their homes due to recent rental reforms. The North of England, Scotland and Wales are expected to be the most resilient regions in the short term. Looking to 2027, it will likely be a slow start to the year, with house price growth picking up when the economic outlook improves.

The risk of overpricing your home

According to a survey by Zoopla, 44% of UK homes on the market failed to sell in the last three years.

The report found that the most common pitfall is pricing homes too high. Of those who failed to sell their home, 34% said that, in hindsight, they were overconfident with the price, but at the time they thought it was reasonable. Meanwhile, 16.2% knew from the outset that they were overshooting their home’s value.

Half (53%) of sellers were only able to find a buyer after lowering the asking price, which highlights the importance of getting a valuation before putting your home on the market. A third (32%) of respondents said they got as far as putting an offer down on a property before they got their own home valued. Some (21%) admitted to overpricing their home so that they could afford to buy a property they had already found.

Coastal property hotspots

House prices in Britain’s seaside towns have continued to climb over the past year, with data from Rightmove revealing the coastal locations experiencing the strongest growth.

Bootle, Merseyside, has emerged as the UK’s top seaside property hotspot for summer 2026, with asking prices rising by 11% on average in the past year to £141,680. Nearby Crosby takes second place, recording a 9% increase to £330,900. The town is well known for its beach and Antony Gormley’s iconic iron men installation.

Wales dominates the rankings, claiming five of the top ten most sought-after seaside locations. Penarth and Llantwit Major both posted annual price growth of 8%, while Porthcawl saw a 6% rise. Bangor, in Gwynedd, also recorded strong growth, with asking prices increasing by 7%.

Scotland has one ranking in the top ten – Helensburgh in Dunbartonshire – where average asking prices have risen by 6%.

Commercial market update

The latest Commercial Market Outlook from Carter Jonas offers an insight into current market trends. The data indicates an uneven recovery in investment volumes, with £10.7bn traded in Q1 2026 – below the higher levels seen in Q4 2025 but slightly above the total for Q1 2025.

The report also notes that transaction activity is increasingly deal-specific, with the office and retail sectors proving to be more resilient than expected. Return-to-office mandates have led to a shortage of prime supply in many key city centre markets as demand continues for high-quality office spaces. This has supported annual rental growth of 3% in April 2026 for all UK offices, according to the MSCI Monthly Index.

The industrial market saw a softer quarter, as demand continues to be shaped by a variety of economic, political and technological factors. More retailers are expected to outsource their operations to third-party logistics (3PLs), which will continue to affect supply chains.

Logistics market overview

A recent report from Knight Frank shows how the logistics market is faring so far this year. The sector saw £1.64bn in transactions in Q1 this year, which is 5% lower than the same period last year.

The outbreak of war in the Middle East has caused a rise in swap rates and alternative asset yields, so investors are now scrutinising deals more carefully. However, they will likely be under pressure to deploy capital and there have still been some significant transactions in Q2.

Occupier take-up reached 9.0 million sq ft in Q1, which is in line with the total for Q4 2025. Meanwhile, the vacancy rate increased to 8.3% due to lower quality second-hand units returning to the market. At the end of Q1, there was 8.3 million sq ft of speculative space under construction across 56 units – this is expected to remain suppressed due to inflationary pressures.

The rise of infrastructure capital

A report from CBRE has highlighted that infrastructure capital has become an increasingly important driver of commercial real estate investment.

In 2025, £29.9bn was invested in the UK Alternative and Living sectors, which includes £13bn into Healthcare. Infrastructure capital accounted for 44% of investment into real estate last year, a sharp increase from 15% in 2016. This trend is expected to continue, with a survey of institutional investors across the globe finding that 98% were expecting to either increase their allocations to infrastructure or keep them the same over the next 12 months.

CBRE notes that investors may be attracted to infrastructure as it can be seen as a more stable asset class than others, as income is often underpinned by long-term government contracts. However, these sectors are also more reliant on government funding which can affect long-term income assumptions. Plus, there can be greater operational complexity, which may impact returns.

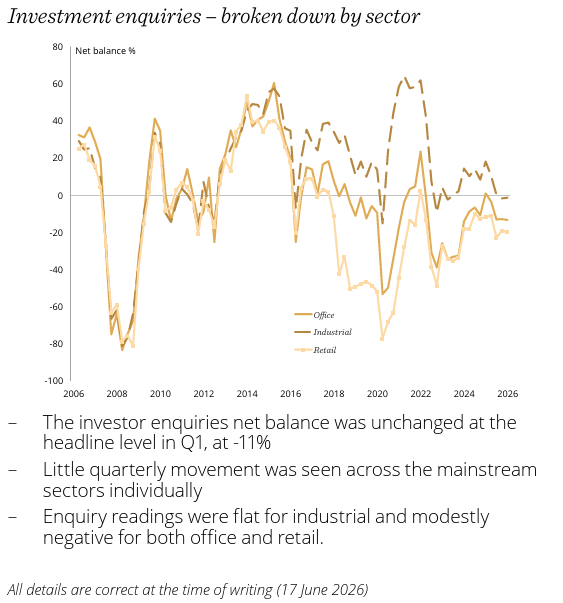

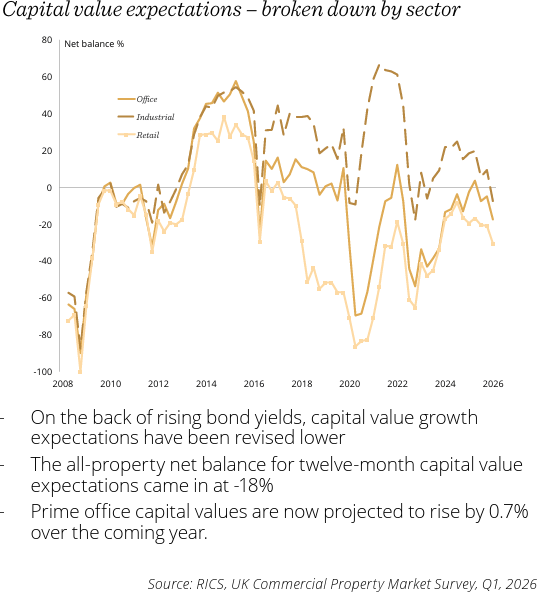

Source: RICS, UK Commercial Property Market Survey, Q1, 2026

Commercial property outlook

All details are correct at the time of writing (17 June 2026)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK.