| Market sentiment – figures show a sharp deterioration in market sentiment as geopolitical tensions rise in the Middle East | BTR investment – figures highlight the resilience of residential rental markets as investors remain attracted to stable income streams | UK house sales – research shows the average house sale period is one day longer than the same time last year |

Geopolitical uncertainty hits confidence

The Royal Institution of Chartered Surveyors (RICS) Commercial Property Monitor for Q1 2026 highlights a sharp deterioration in market sentiment as geopolitical tensions weigh on investor confidence.

Survey respondents pointed to rising energy costs, inflation concerns and higher bond yields as key pressures affect the sector. Most notably, the credit conditions indicator fell sharply to -44%, down from +9% in Q4 2025, marking the weakest reading since 2023.

While investment activity has softened and expectations for capital values have weakened, occupier demand has remained relatively stable. Prime office and industrial rents are still forecast to grow modestly over the next year, particularly in London, although projections have been revised down. Alternative sectors such as data centres, life sciences and aged care continue to outperform traditional markets.

Overall, the report suggests that commercial property recovery is losing momentum amid growing economic uncertainty and tighter financing conditions.

BTR investment holds strong

Investors committed around £679m to acquiring or funding Build-to-Rent (BTR) assets during Q1 2026, demonstrating continued confidence in the sector.

Knight Frank figures highlight the resilience of residential rental markets as investors remain attracted to stable long-term income streams and sustained tenant demand.

Although higher borrowing costs and geopolitical tensions have created more cautious conditions across the wider property market, BTR continues to benefit from structural undersupply in UK housing and strong rental growth. Institutional investors are particularly focused on high-quality schemes in major regional cities and London, where demand for professionally managed rental accommodation remains robust.

The sector’s appeal is also supported by changing lifestyle trends, affordability pressures in the sales market and the growing preference for flexible urban living. While transaction activity across commercial real estate has slowed, the strong level of BTR investment suggests it remains one of the most attractive areas of the UK property market.

Quality drives UK holiday let market

The UK holiday accommodation sector has remained resilient despite economic pressures, regulatory changes and evolving consumer habits, say Savills.

While overall demand remains stable, travellers are increasingly selective, with shorter stays, later bookings and higher expectations. Rather than compromise on quality, guests prioritise premium accommodation and experience-led breaks, helping high-quality operators maintain strong occupancy levels.

The report highlights changing trends, particularly among DINKYs (dual-income, no kids yet), who are driving demand for short breaks focused on wellness, dining and personalised experiences. Multigenerational travel is growing, with families seeking spacious accommodation and onsite amenities suited for all ages.

Operators also face rising regulatory and operational pressures, including changes to short-term let licensing and business rates. Looking ahead, the sector is expected to favour businesses that can combine high standards with flexible, experience-focused offerings while adapting to an increasingly complex operating environment.

Cautious confidence in the housing market

Savills’ latest UK Housing Market Update highlights a market that remains active but increasingly cautious as buyers and homeowners respond to economic uncertainty and higher borrowing costs.

While mortgage activity has stayed relatively resilient up 1.3% from February, many households are acting quickly to secure deals before any further increases in interest rates. At the same time, surveyors and market indicators point to slowing momentum, with buyer demand softening and unsold stock beginning to rise.

Savills note that inflation concerns and geopolitical uncertainty continue to influence the Bank of England’s approach to interest rates, creating a more careful environment for both buyers and sellers. Regional differences are also becoming more pronounced, with some areas continuing to see stronger demand than others. Overall, the update suggests the market is showing resilience, but that affordability pressures and cautious consumer sentiment are likely to temper activity in the months ahead.

Landlords exit rental market

New research by Savills shows that around 700 former rental homes are being listed for sale every day across Britain, reflecting growing pressure on private landlords as regulation tightens.

The data shows that approximately 254,000 previously rented properties were put up for sale in the year to March 2026, a 9% annual increase and 28% higher than two years ago.

The Renters’ Rights Act is a major factor behind the trend. Lucian Cook, Savills’ Head of Residential Research said the legislation has become “a clear point at which to reassess” investment decisions, particularly for smaller landlords facing higher mortgage costs and tougher energy-efficiency requirements.

The reforms include the abolition of Section 21 ‘no-fault’ evictions and the introduction of periodic tenancies, measures designed to strengthen tenant protections. However, concerns remain that a shrinking supply of rental homes could place further pressure on renters in already competitive markets.

Average sale time holds at 33 days

The UK housing market continues to hold steady despite concerns over conflict in the Middle East, rising mortgage costs and weaker consumer confidence.

Research from Zoopla shows the average time to sell a home is now 33 days, just one day longer than the same time last year, suggesting committed buyers and sellers are still moving ahead with transactions.

Zoopla’s data also found that agreed sales are running only 3% below last year’s levels, while buyer demand has rebounded since Easter as lenders begin easing mortgage rates. However, the market remains uneven across the country. London and southern England are seeing slower activity, particularly in areas reliant on first-time buyers facing affordability pressures and higher Stamp Duty costs.

Richard Donnell, Executive Director at Zoopla, said the figures show “people who need to move are getting on with it” despite ongoing uncertainty.

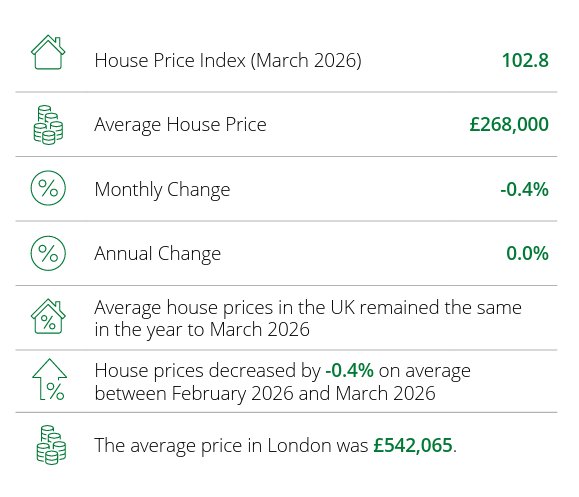

House price: Headline statistics

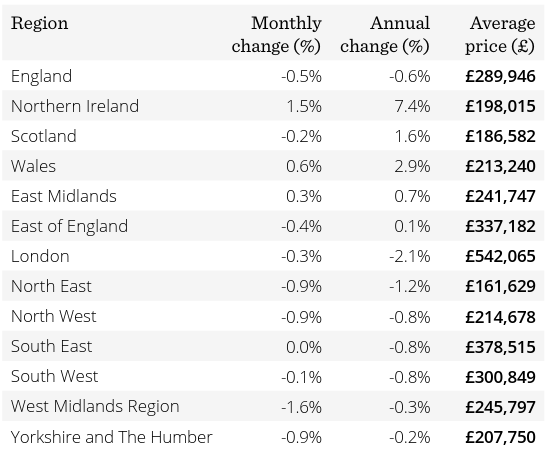

House price: Price changes by region

All details are correct at the time of writing (20 May 2026)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK.